Understanding the Fiduciary Standard

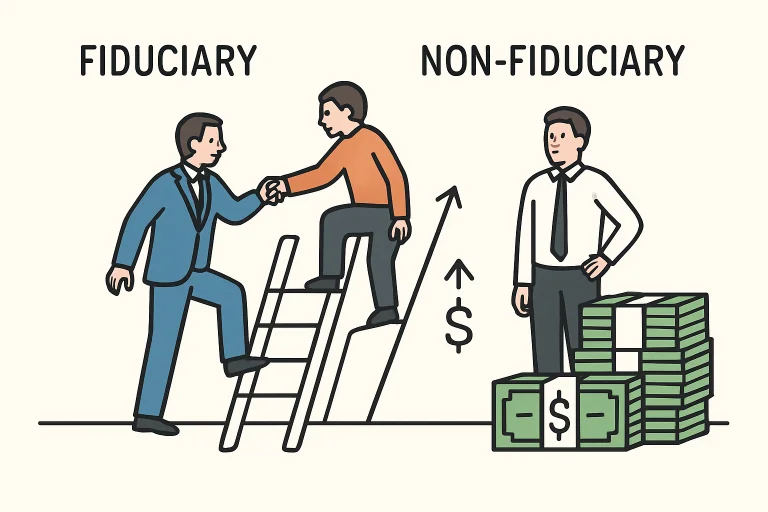

Entrusting your finances to a professional is a significant decision, and understanding which ethical and legal standards they follow is key. The fiduciary standard represents the highest level of care in the financial industry, requiring advisors always to put their clients’ best interests ahead of their own. This rigor ensures strategies and advice are optimally tailored for each client, free from outside influence or self-enrichment of Fiduciary Standards.

Fiduciary advisors must act with loyalty, care, and full transparency, disclosing potential conflicts of interest. This standard goes beyond simply following the law—it establishes a relationship of trust, aligning a client’s financial success with the advisor’s ethical responsibility. The difference between fiduciary and non-fiduciary advisors is pivotal, as not all finance professionals are held to this higher bar. Because financial outcomes and the risk of hidden incentives can greatly affect your wealth, understanding who is bound by the fiduciary standard can safeguard your financial future.

Different Standards Among Financial Professionals

Financial professionals operate under varying standards, which are sometimes determined by their job titles and regulatory oversight. For instance, investment advisers registered with the SEC are legally required to act as fiduciaries, but broker-dealers are typically held only to a suitability standard. Under this lesser benchmark, their recommendations must be suitable—but not necessarily optimal—for their clients, and they are not required to put client interests ahead of their own profits.

This distinction can lead to blurred lines and confusion about the advisor’s true loyalties. Broker-dealers may recommend products that provide higher commissions even if other options would be more suitable for the client’s needs. Meanwhile, fiduciary advisors are compelled by law and ethics to recommend what is genuinely best for the client, making it important to verify the advisor’s official obligations before engaging their services of Fiduciary Standards.

One story leads to another—find more gems inside our Related Posts now!

The Importance of Fee Structures

Fee structure is another crucial factor that can shape advice and impact outcomes. Advisors compensated through commissions might be incentivized to sell certain investment products or services, potentially clouding the objectivity of their recommendations. For example, a non-fiduciary advisor may push high-fee mutual funds or insurance products that pay higher commissions, regardless of whether they are ideal for a client’s investment objectives.

Conversely, fee-only fiduciary advisors typically charge a fixed rate or percentage of assets under management, directly aligning their compensation with their client’s success and promoting greater transparency. Fee-only models often eliminate many of the conflicts of interest that could otherwise bias the advice a client receives. Understanding these differences can help clients evaluate if their advisor’s guidance is impartial or potentially influenced by compensation arrangements.

Regulatory Landscape and Its Impact

Regulation is essential in shaping how money managers and financial professionals serve their clients. Efforts like the U.S. Department of Labor’s fiduciary rule sought to ensure that anyone who offers advice for retirement accounts must act as a fiduciary. While this rule was partially implemented before being rolled back, its intent remains a point of debate, with new proposals and adjustments emerging regularly to address gaps in investor protection for Fiduciary Standards.

Investors should stay informed about these regulatory changes and seek professionals who adhere to the most rigorous standards, regardless of legal requirements, to protect their interests better and limit exposure to conflicted advice.

Identifying Fiduciary Advisors

Determining whether an advisor is a fiduciary requires research and due diligence. Here are key steps you can take:

- Ask Directly: If possible, ask if the advisor always acts as a fiduciary and get their answer in writing.

- Review Credentials: Professional designations such as Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA) demand adherence to fiduciary standards or their ethical equivalents.

- Examine Fee Structures: Opt for advisors who are fee-only, minimizing commission-based conflicts.

Benefits of Working with a Fiduciary

- Trust and Transparency: Fiduciaries must fully disclose fees, conflicts of interest, and relevant background information for every recommendation, instilling greater confidence in your financial partnerships.

- Client-Centric Advice: Because fiduciaries must act in your best interest, recommendations will likely be tailored to your unique goals, risk tolerance, and long-term financial plans.

- Long-Term Relationship: Since their compensation often grows alongside your portfolio, fiduciaries are motivated to build relationships that succeed over time, rather than short-term product sales.

Potential Drawbacks and Considerations

- Cost: Fee-only advisors may charge higher up-front fees, which can pose a barrier to entry for smaller investors or those just beginning to build wealth.

- Availability: Many fiduciary advisors have account minimums, sometimes making their services inaccessible to investors with limited assets. Before deciding, it is crucial to inquire about minimums and service tiers.

Making an Informed Decision

Choosing a financial advisor can have lasting implications for your financial security and peace of mind. By understanding the fiduciary standard, knowing how different professionals are regulated, and carefully examining compensation structures, you can better assess who is truly positioned to serve your best interests. Always research your advisor’s background, ask direct questions about their fiduciary duties, and seek those who prioritize transparency and client-focused advice.

Curiosity never sleeps! Explore More and keep your mind inspired daily.