Bank of Japan Governor Kazuo Ueda, during a meeting in Nagoya on Monday, December 1, 2025, delivered what many analysts consider the most critical speech of recent years for currency markets and beyond. The central bank will examine the pros and cons of a rate hike Yen Carry Trade at the meeting on December 19.

Japan has maintained interest rates near zero for almost 30 years, oscillating between persistent deflation and economic stagnation; its policy has never changed.

Due to this, such a declaration moved the markets and represents much more than a simple monetary policy announcement.

Take the next step—discover insights in this related content.

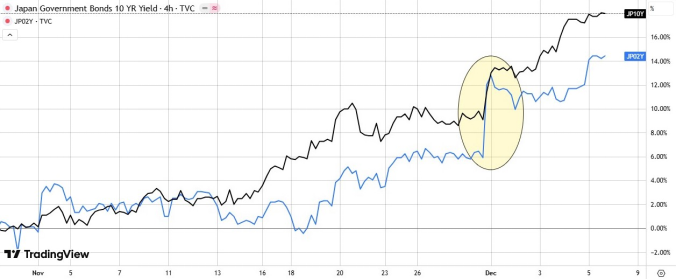

Figure 1. In the figure, the increase in Japanese 2- and 10-year yields immediately after Ueda’s declaration on December 1, 2025, reaching highs not seen since June 2008.

The BOJ intends to reassure markets by gradually normalizing these exceptionally accommodative conditions, avoiding sharp turns toward restrictive policies.

On the other side, they walk on a razor’s edge; delaying a rate hike too long could unleash inflation and force the central bank to intervene drastically in the future Yen Carry Trade, with all the negative consequences.

Currently, traders are pricing a 76% probability of a rate hike at the December 19 meeting and a 94% probability by January.

On Monday morning, following Ueda’s statements, the USD/JPY exchange rate also plummeted by over 100 pips.

Figure 2. The collapse of the USD/JPY exchange rate after Ueda’s declaration on December 1, 2025.

Currently, USD/JPY is hovering around 155, a level that represents a crucial technical point.

On the one hand, the growing expectation of a Federal Reserve rate cut in December is exerting downward pressure on the dollar, with traders now pricing an 88% probability that the Fed will cut rates by 25 basis points this week.

On the other hand, as we have already said, the BOJ is moving in the opposite direction, with possible rate hikes.

It follows a tightening of the rate differential between the USA and Japan. A differential, which is the key factor in the weakening of USD/JPY or Yen Carry Trade. For decades, the wide differential (currently around 3.7%) has made it highly profitable to borrow yen and invest in dollars, a phenomenon known as the “carry trade.” Now that this gap is closing, the entire logic of the carry trade is being put into question.

To fully comprehend why the USD/JPY is so important and why its movements can significantly impact global markets, it is essential to understand the carry trade mechanism in depth.

The carry trade is a straightforward strategy that leverages interest rate differentials between countries. For example, a trader borrows 100 million yen at 0.5% and converts them into dollars, then invests those dollars in US Treasury bonds that yield 4.2%. The difference, about 3.7%, is the profit minus hedging costs.

However, the true power of the carry trade emerges when one scales it with leverage. Amplified with leverage, modest rate spreads become real money, with annualized returns that can hover between 5% and 6%. No one knows or manages to precisely estimate how many trillions of dollars have ended up in carry trade operations.

The beauty (and the danger) of this strategy lies in its dependence on two fundamental conditions: Japan must maintain its accommodative monetary policy for Yen Carry Trade, and the yen’s exchange rate must remain stable or depreciate against major currencies.

As long as the yen remains weak and volatility remains low, the trade is profitable. However, if the yen strengthens suddenly, or if the BOJ were to intervene due to an overly devalued yen, the consequences could be devastating.

The so-called “unwinding of the carry trade” is a systemic event that can shake the entire global financial system.

Investors are forced to sell what they possess and repurchase yen to repay their loans, regardless of the type, from cryptocurrencies to stocks. The carry trade is therefore a mechanism that models global liquidity; the unwinding of it drains enormous quantities in a very short time.

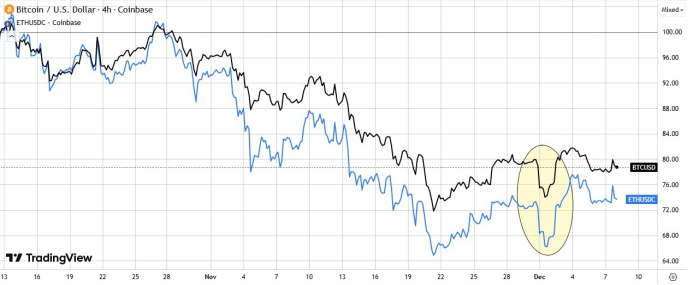

The increase in JGB yields to highs since 2008 (as seen in Figure 1) is already breaking the low-cost yen financing that many traders used for leveraged positions, causing a reverse-carry effect reverberating on global risk assets, with cryptocurrencies leading the way. As a result, liquidations of two major players — BTCUSD and ETHUSD — were witnessed.

Figure 3. Chart of BTCUSD and ETHUSD, strong liquidations on December 1, 2025.

The real reason the BOJ finally feels secure in raising rates lies in a structural transformation of the Japanese economy that has taken decades: the end of wage deflation. After thirty years of stagnant wages, Japan is seeing an average increase of 5.46%, the largest in 30 years. This is an extraordinary number for Japan, a country where, for generations, workers had accustomed themselves to minimal or even negative wage increments.

But we are discussing nominal wages Yen Carry Trade. Unfortunately, high inflation erodes these wage increases, and in 2024, Japanese workers experienced a loss of purchasing power, with real salaries decreasing by 0.2%.

In November 2025, nominal hourly wages increased by 3.5% on an annual basis, marking 26 consecutive months of growth. The positive trend appears to be solid and not just a temporary phenomenon.

However, inflation remains stubbornly above the BOJ target. Tokyo core inflation is currently at 2.8% year-over-year, well above the 2% target.

If companies continue to offer substantial wage increases in spring 2026, the BOJ will have confirmation that Japan has finally exited the deflation trap and will have the margin to increase interest rates to try to reduce inflation.

In conclusion, Japan is currently at the forefront of global liquidity, and the first half of 2026 will be critical for the BOJ and Fed’s decisions on monetary policy.

The unwinding of 30 years of carry trade is at the center of market concerns, and all risk assets are potentially involved.

The Fed’s will to cut rates goes against the BOJ, which is preparing to raise them. Currently, the levels are not concerning; however, if the differential between rates were to fall below 3% by mid-2026, the carry trade would become significantly less attractive, and we would likely witness aggressive liquidations.

The following data on labor, wage increase, and Japanese inflation will mark the road of the BOJ. If the yen continues to devalue and the wage trend confirms itself, the BOJ could feel more secure in increasing rates; the way and the speed with which it does so will mark the destiny of world financial markets.

Go beyond the page—explore additional content curated at 2A Magazine for you.